Virginia just crossed a threshold almost no one has named.

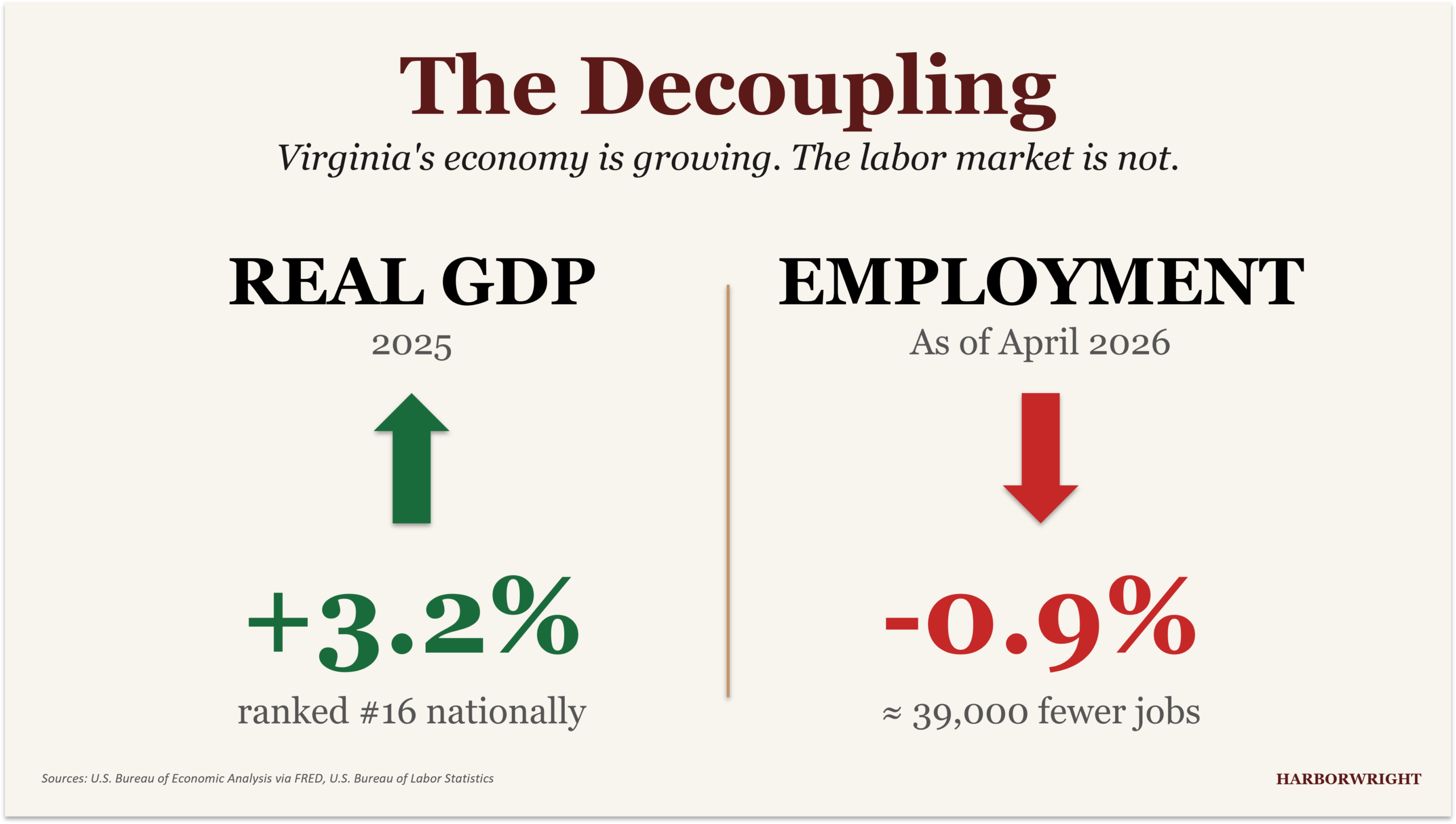

In 2024, the Commonwealth produced more output than at any point in its history. Real GDP climbed 3.1%, faster than half the country. Personal income jumped 5.5%, with a Q4 gain that ranked 4th nationally. By every headline metric, Virginia is winning.

And yet, 18 months later, fewer Virginians have a job.

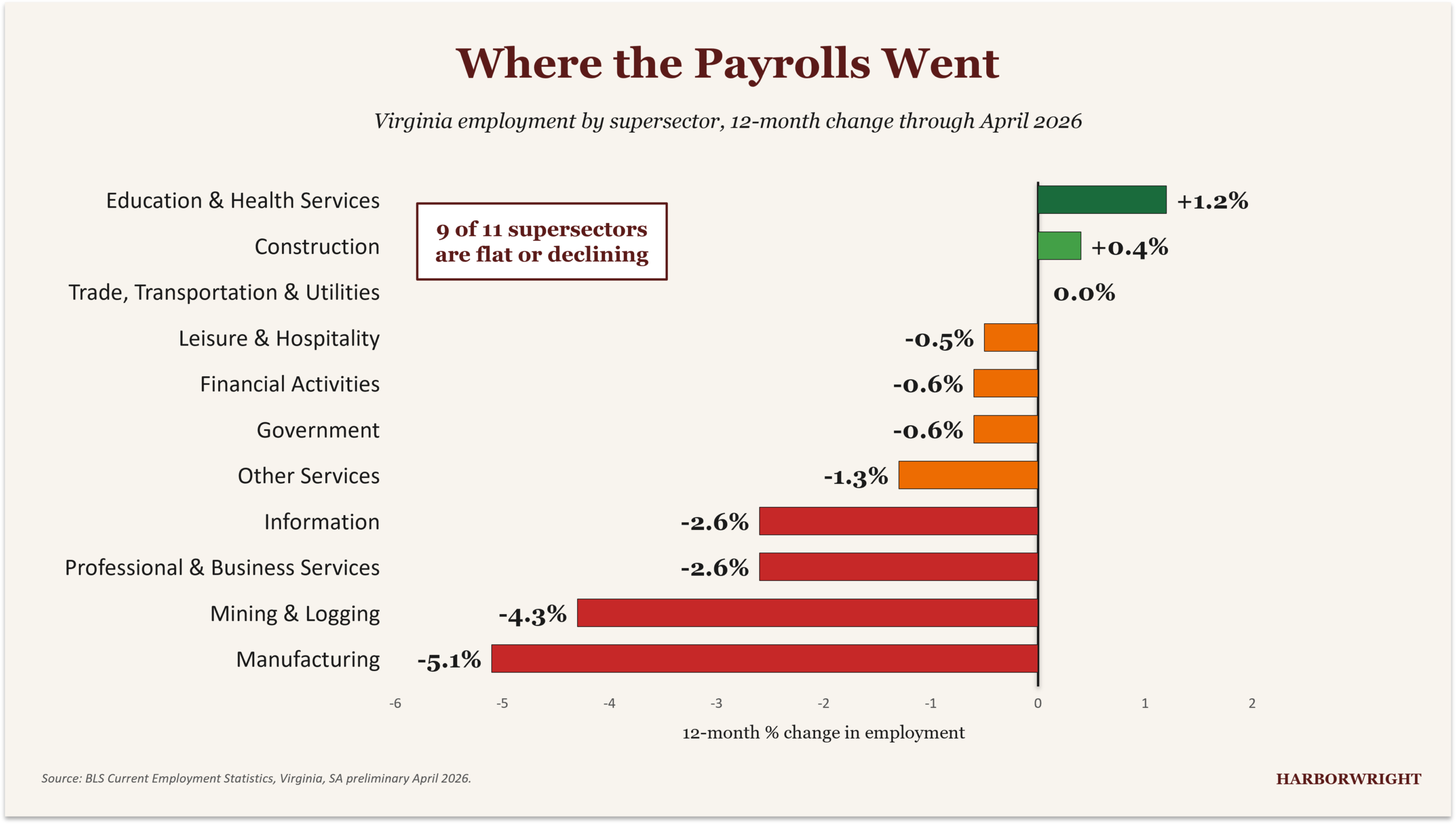

Employment is down 0.9% year-over-year. 9 of 11 industry supersectors are losing jobs. Federal workers have lost 23,500 positions in 11 months, wiping out 6 years of growth. Manufacturing has shed 5.1% of its workforce. Information jobs, the sector that includes Virginia’s celebrated data center cluster, are down 2.6%.

The economy is growing. The labor market is not.

That gap is the most important economic story in the Commonwealth right now, and it has a name: data centers, the workers they don’t hire, and the counties figuring out what to do with the money they generate.

The Virginian Economy

By every standard signal, Virginia in 2024 was a state on the move.

Real GDP, the broadest measure of the goods and services Virginia produced, climbed 3.1% to $616B in chained 2017 dollars, the strongest reading in 3 years. Nominal GDP reached $764B. Virginia ranked 16th among the 50 states for real GDP growth, and accelerated into Q4 with a 3.4% annualized expansion that ranked 10th nationally.

Personal income, the broadest measure of what Virginians earned, rose 5.5% on the year. In Q4 alone, Virginia posted the 4th-largest personal income gain in the country. The Bureau of Economic Analysis singled out professional, scientific, and technical services as the leading contributor.

Weekly wages followed. Through Q3 2025, the average covered worker in Virginia earned $1,504 a week, up 4.2% year-over-year. That ranked 10th nationally by level.

These are not the numbers of a state in trouble.

And yet by April 2026, total nonfarm payrolls in Virginia stood at 4,245,900, down 0.9% from a year earlier. The unemployment rate had drifted up from 3.6% to 3.8%. Of the 11 industry supersectors that the Bureau of Labor Statistics tracks, only 2 added workers over the past 12 months.

When output rises and headcount falls, somebody is doing more work for less. Or somebody is doing none.

Where the Growth Went

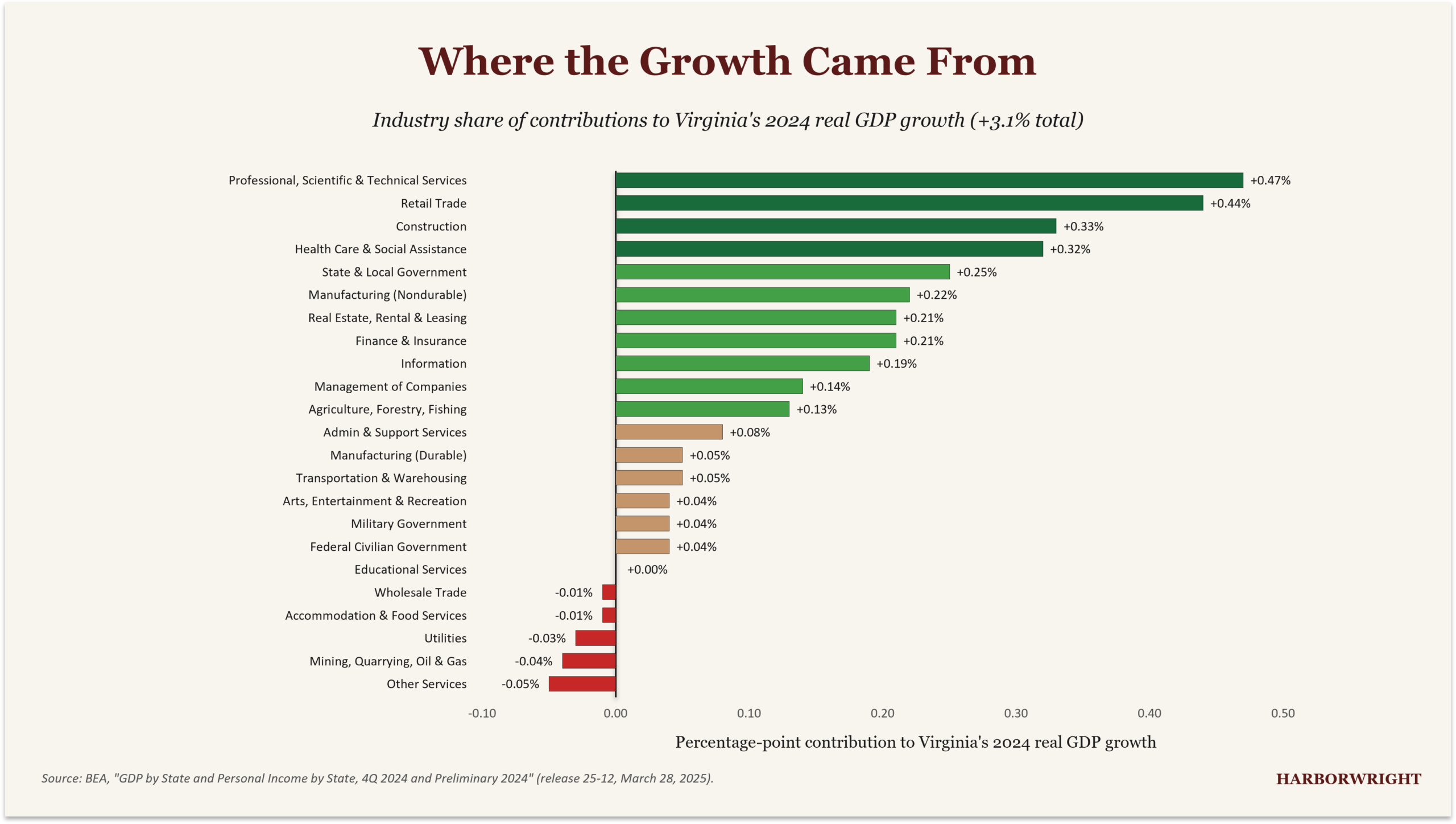

The BEA breaks Virginia’s 2024 real GDP growth into 22 industry contributions, each a share of the total expansion. The leaders tell a familiar Virginia story.

- Professional, scientific, and technical services contributed 0.47% to growth, the single largest industry contribution. This is the consulting, engineering, federal-IT, and government-contracting backbone of Northern Virginia.

- Retail trade contributed 0.44%, an unusual position for a sector usually treated as cyclical filler.

- Construction contributed 0.33%, reflecting the data center building boom and continued housing activity in Henrico, Loudoun, and Prince William.

- Health care and social assistance contributed 0.32%, the steady expansion that has defined the post-pandemic period in every state.

- Manufacturing contributed 0.27%, almost entirely from nondurable goods (0.22%). Durable goods added only 0.05%.

- State and local government contributed 0.25%. Real estate added 0.21%. Finance and insurance added 0.21%. Information added 0.19%.

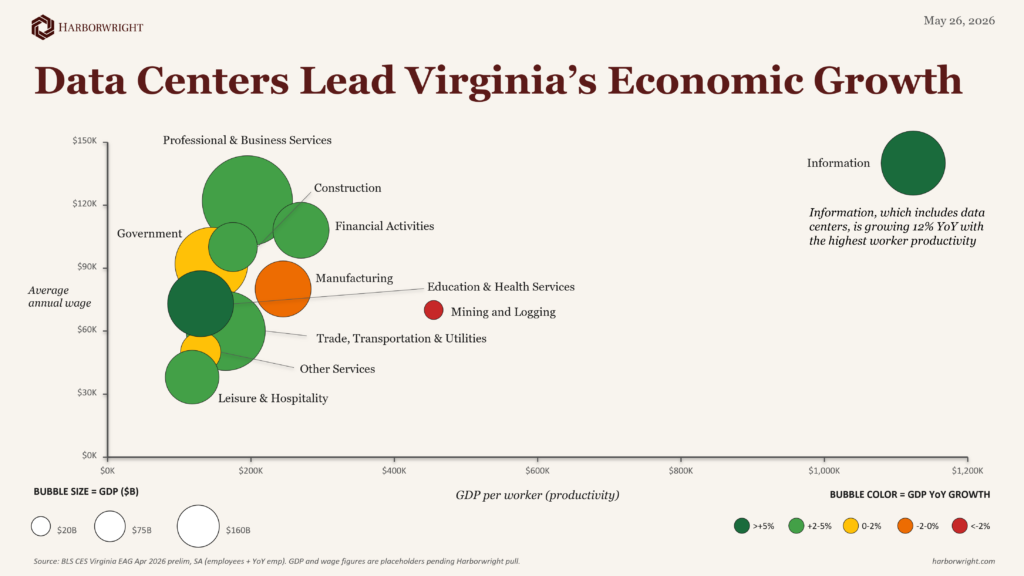

The pattern: capital-intensive activity (data centers, real estate, construction) and services that scale through revenue rather than headcount (consulting, finance, information) carried the growth. Sectors that depend on adding workers to add output did less.

The Data Center Story

Information sector employment is shrinking. Information sector output is not. The two facts do not contradict each other if you understand what Virginia’s data center industry actually is.

NAICS 51, the formal name for “Information,” covers telecommunications, software publishing, broadcasting, motion picture, and one category that dominates Virginia’s footprint: NAICS 518, Data Processing, Hosting, and Related Services. That is the industrial code data centers live under.

The aggregate scale is what makes Virginia distinctive. As of late 2024, the Commonwealth hosted roughly 340 data center buildings. Together they drew 5 GW of electricity, equivalent to roughly 29% of Dominion Energy’s current system peak demand. JLARC’s December 2024 study estimated the industry contributes $9.1B to Virginia’s GDP, $5.5B in labor income, and 74,000 jobs. JLARC also flagged a caveat the press releases rarely repeat: most of those jobs are construction-phase, not operational.

The Balancing Act

The data center economy has a binding constraint, and it is tied to electricity.

Dominion Energy’s 2024 Integrated Resource Plan projects peak load growth from 17,131 MW in 2022 to 28,963 MW by 2045, a 70% increase and the largest sustained demand growth in the utility’s history. Dominion expects data center peak demand alone to reach roughly 9 GW within 10 years, a 25% increase on top of the utility’s current total system peak.

Building that capacity requires generation, transmission, substations, and right-of-way, all on timelines measured in decades. It also requires a cost-allocation framework that does not push the bill onto residential ratepayers who did not vote for the load.

The State Corporation Commission moved on that question in November 2025, creating a new GS-5 rate class specifically for hyperscale customers (loads above 25 MW with load factors above 75% and 14-year contract terms). The structure is designed to recover infrastructure costs from the customers driving them.

The 2026 General Assembly session went further. SB 253 / HB 1393 would shift additional cost to data center customers. The SCC’s preliminary analysis suggested a 3.4% rate decrease (roughly $5.52 per month) for a typical residential customer and a 15.8% rate increase for data center customers. Governor Spanberger amended the bill in April to soften the explicit cost-shift and to add a 9.3% return-on-equity cap, with overages refunded.

A separate proposal (HB 1515) would have imposed a temporary moratorium on data center approvals in localities with unfulfilled energy connection requests. It was carried over to the 2027 session.

The question is not whether data centers will keep coming to Virginia. The infrastructure is here, the workforce knows the playbook, and the customers want capacity. The question is who pays for the grid the next generation of data centers will run on.

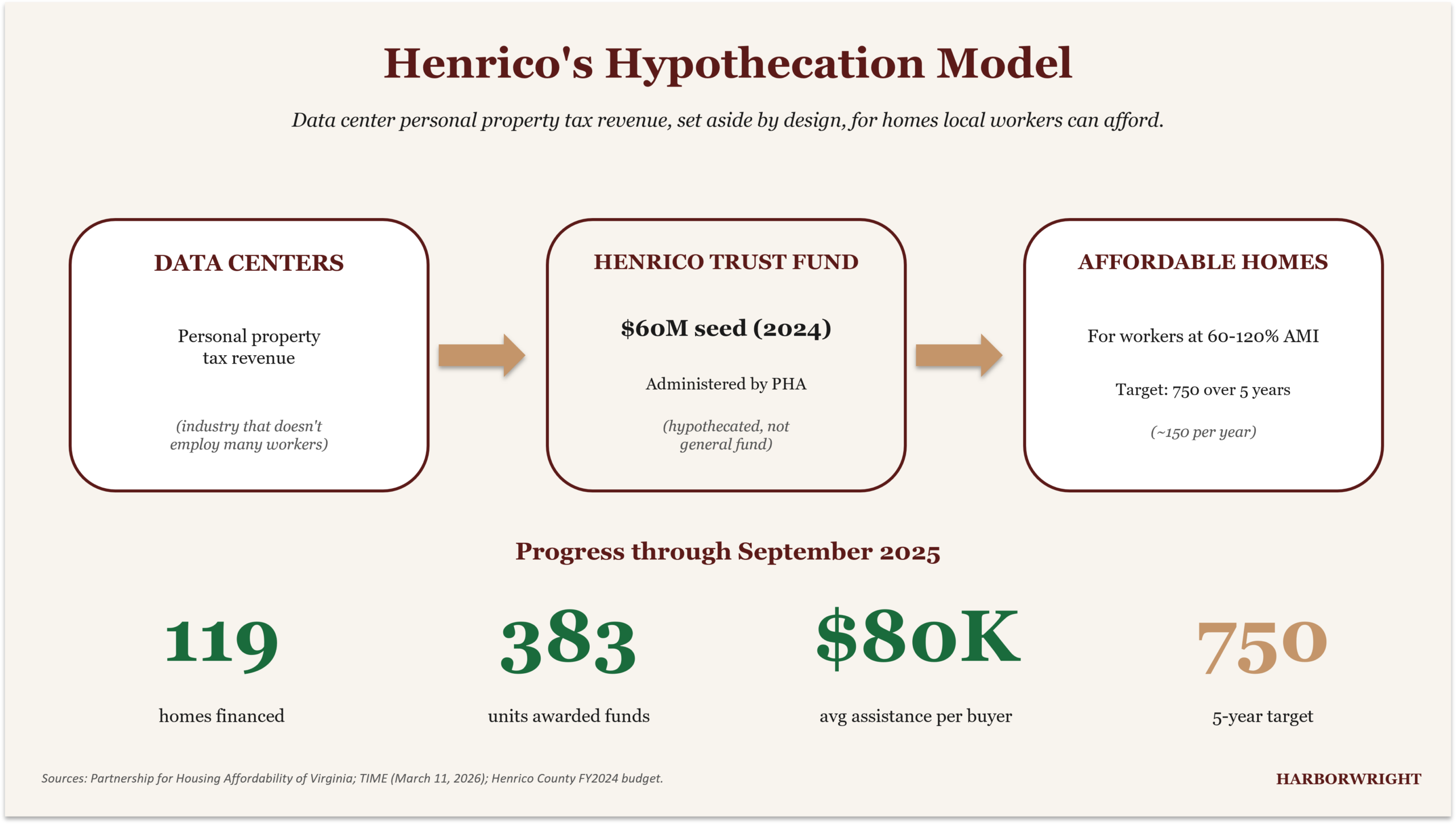

The Henrico Model

There is one Virginia county that has answered a different question: not how the grid gets paid for, but what the data center money should buy.

In 2024, Henrico County established the Henrico Affordable Housing Trust Fund, seeded with $60M from data center personal property tax revenue. The fund is administered by the Partnership for Housing Affordability, a Richmond-region nonprofit that has been working housing issues since 2003.

The goal is 750 affordable homes over 5 years, roughly 150 per year, targeting buyers at 60% to 120% of area median income. Through September 2025, the fund had financed 119 completed homes, had 7 more under contract, and had awarded funds toward 383 affordable units across 2 years. The 30 closed buyers received an average of $80,000 in assistance each.

Henrico did not put data center revenue into the general fund. Henrico hypothecated it: the money that comes from the industry that doesn’t employ many local workers is set aside, by design, for homes that local workers can actually afford.

Loudoun County has set aside $7.4M from a $250M general-fund surplus largely attributable to data center revenue, with $17M proposed for the next budget cycle. Prince William County operates a $16M affordable housing loan fund with a commitment of $5M per year in tax revenue from FY2024 through FY2029, totaling $31M. Neither program is structured as cleanly as Henrico’s.

The Henrico model is replicable. Any jurisdiction with a data center pipeline could do the same. The only thing required is the political decision to convert the industry’s revenue into the workforce housing the industry’s growth obscures.

The Outlook

Three things will determine which version of Virginia’s economy emerges from the rest of the decade.

- Federal civilian employment. The Commonwealth has roughly 350,000 federal civilians, more than half in Northern Virginia, and the past 11 months have shown how fast that base can erode. A second year of comparable cuts would push Virginia’s labor market into measurable contraction.

- Data center economics. If residential ratepayers absorb a meaningful share, the political coalition that supports the industry will fray.

- Replication of the Henrico hypothecation model. The structural argument for it is straightforward: an industry that generates extraordinary revenue without generating proportionate employment has to fund a community benefit, or it will eventually generate a political backlash that constrains its own future.

The macro picture is the one Virginia’s leadership now has to govern around. The economy can grow without the labor force growing. The politics of that gap is the next decade’s story.

Sources

- Real GDP and personal income figures are from the Bureau of Economic Analysis, “Gross Domestic Product by State and Personal Income by State, 4th Quarter 2024 and Preliminary 2024” (BEA news release 25-12, March 28, 2025). Industry contributions reflect BEA’s 22-industry breakdown.

- Employment data are from the Bureau of Labor Statistics, Current Employment Statistics, Virginia state-level seasonally adjusted series through April 2026 (preliminary).

- Wage data are from BLS Quarterly Census of Employment and Wages, Q3 2025 (preliminary).

- Federal job loss figures are from VPM News and Virginia Center for Investigative Journalism reporting, January 2026.

- Data center industry estimates are from JLARC, “Data Centers in Virginia,” December 9, 2024. Dominion load projections are from the 2024 Integrated Resource Plan as summarized by Virginia Mercury (October 22, 2025) and the E3 analysis attached to the JLARC report.

- Henrico Affordable Housing Trust Fund figures are from the Partnership for Housing Affordability and TIME magazine reporting, March 11, 2026.